It’s time to shine at your next Braai!

I felt that this is the most appropriate name for this article for multiple reasons. Many of the conversations around me are about the current uncertainty. Vaccines and Covid are no longer the talk of the town. It was replaced with inflation, recession, and the Crypto Crash of 22. We want to start by saying that we don’t have a crystal ball, we don’t have all the answers, nor do any other humans on this planet. We are all making educated deductions based on the information we have on hand and historical trends. Unfortunately, some assumptions are less educated than others, but that’s what makes capital markets such an opportunity. This article has evolved, and I cannot communicate it all in one message. We believe this will take at least three instalments, possibly even five but let’s get to the point.

Interest Rates

This week the SARB Monetary Policy Committee increased the Repo Rate to 4% from 3.75%, this was in line with expectations and should not be any cause for alarm. Expectations are that the US Fed will most likely make three rate increases in 2022 of 0.25% each, and the announcement of this was a catalyst for the recent selloff in the markets, most notably in growth stocks. The US does need to normalize interest rates, and this will be a step in the right direction. However, it has sparked much debate and volatility in the US market. The conversation is clearly about the sudden rise in US Inflation combined with rising interest rates and the possibility that the US fall into a recession.

Risk vs Volatility

I want to start with the concept of Risk vs Volatility. Many people get these two confused or even think that they are the same thing, they are not. Volatility is defined as the frequency and magnitude of market movements up and down, while the risk is defined as the potential for permanent loss of capital. An increase in volatility does not directly impact the risk of a portfolio from suffering a permanent capital loss, but it does get everyone’s attention and generally brings on the fear of loss. If the investment thesis is still sound and the global system has not suffered some form of fundamental change, then the chances of permanent capital loss are extremely small. Any equity portfolio, index or indices will have times of calm, gains and losses, which is why the stock market is not recommended for investors with less than a 5-year investment horizon. It is the nature of the portfolio that determines the volatility and the risk, but that is a whole different conversation.

As I mentioned at the start, we need to talk about inflation.

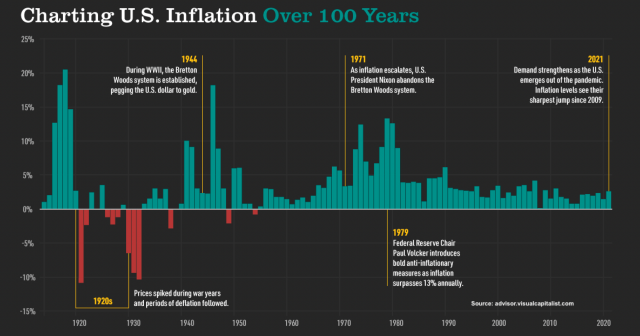

Inflation:

By now I am sure you have had a hundred conversations about inflation, you see it on tv and read about it all over social media and various news agencies. Is this inflation story real and is it a serious problem? It certainly is real but we need to look through the numbers to see the real story, only then can we get meaningful insight into the longer-term implications. Let’s start with the complexity of this current bout of inflation.

US inflation numbers are currently over 6% which is the highest in almost 50 years (sounds scary) but it’s nowhere near the levels seen in the 70’s, not even half of that number (which was over 13%). US inflation has in fact trended lower from 5.4% in 1990 it ranged mostly between 4% & 2% until 2009 when it was 3.8%. That was the start of Quantitative Easing (QE) due to the GFC (Global Financial Crisis) and inflation slowly slid down to about 1.8% in 2019. Most people assumed that QE would cause a marked increase in inflation but this never really come through in the numbers. QE literally puts money back into the pocket of the general population, if we spend this “free money” this is good for the economy and creates jobs (this was the intention of QE) but what has actually transpired is a massive shift in the collective mindset of Americans. Instead of spending the additional funds on consumption, Americans have been saving. This unexpected outcome is most likely still some PTSD from the 2009 crisis which resulted in a whole generation having to restart as they lost their very leveraged property portfolios and eventually their homes. Another factor keeping inflation down has been technology, as it rapidly advances we are able to get things done much faster for a lot cheaper. This downward deflationary pressure allows businesses to be more profitable (higher productivity at lower costs). There is now an entire sector of “Tech” companies who don’t need large offices or labour and they can sell 10x more products with an almost zero increase in cost. These factors reduce living costs for the man on the street, it also pushes up job creation but more on that in a future chapter.

Since Covid we saw multiple months of almost zero inflation as the world ground to a halt and we all got fat in our pajamas.

This is where it all gets interesting. Since late 2020 global economies have been out of synchronization as each territory dealt with its own waves, lockdowns and variants. China, Europe & the US have not had an opportunity to all move forward at the same time which has wreaked additional havoc on an already broken global supply chain. delivery for certain durable goods can be anywhere from 6 months to many years, whilst these products were available “on the shelf” just 2 years ago.

And that’s where we will leave it for today, next time we look into the current status of supply chains, global demand and the impact on inflation numbers.